Different Economic Systems

In order to solve the basic economic problem of scarcity, economic systems emerge or are created by different economic agents within the economy.

-- These agents include consumers, producers, the government, and special interest groups (e.g. environmental pressure groups or trade unions).

--Any economic system aims to allocate the scarce factors of production.

The three main economic systems are a (free) market system, mixed economy, and planned economy.

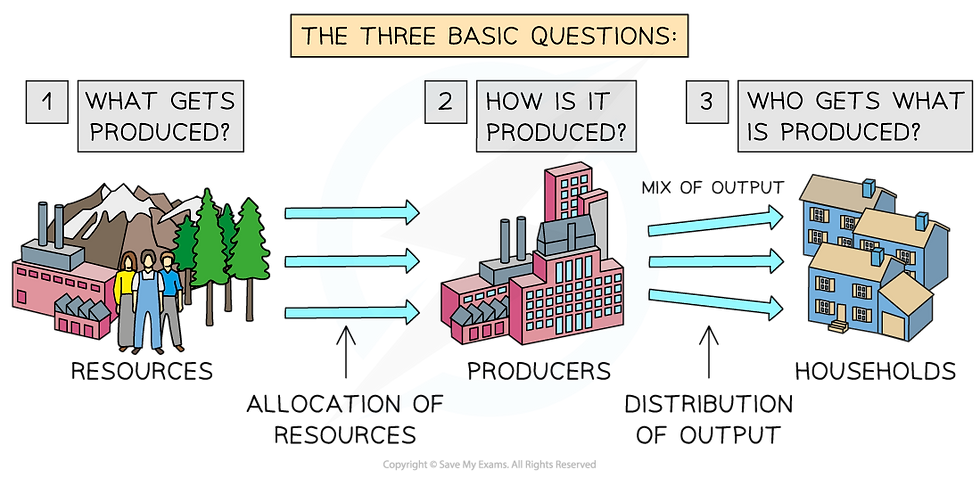

How the three questions are answered determines the economic system of a country

Economic decisions need to be made to answer three important questions:

1. What to produce?

As resources are limited in supply, decisions carry an opportunity cost. Which goods/services should be produced? e.g. better rail services or more public hospitals?

2. How to produce it?

Would it be better for the economy to have labour-intensive production so that more people are employed, or should goods/services be produced using machinery?

3. For whom are the goods and services to be produced?

Should goods/services only be made available to those who can afford them, or should they be freely available to all?

How These Questions Are Answered Determines the Economic System

How a Market System Works ?

A market system works to allocate scarce resources efficiently, purely through the forces of demand and supply (the price mechanism).

-- There is no government intervention in a pure market system (no taxes or government spending).

-- Markets can be physical (e.g. McDonald's) or virtual (e.g. eBay).

The price mechanism is the interaction of demand and supply in a free market

-- This interaction determines prices, which are the means by which scarce resources are allocated between competing wants/needs.

The price mechanism fulfils several functions in an economy:

--Prices allocate (ration) scarce resources.

When resources become scarcer the price will rise further. Only those who can afford to pay for them will receive them.

If there is a surplus, then prices fall and more consumers can afford them.

--Prices provide information to producers and consumers where resources are required (in markets where prices increase) and where they are not (in markets where prices fall).

--When prices for a good/service rise, it incentivises producers to reallocate resources from a less profitable market to this market in order to maximise their profits.

Falling prices incentivise reallocation of resources to new markets

Market Equilibrium and Disequilibrium

Equilibrium in a market occurs when demand = supply.

At this point, the price is called the market clearing price.

--This is the price at which sellers are clearing their stock at an acceptable rate.

A graph showing a market in equilibrium with a market clearing price at P and quantity at Q

Any price above or below P creates disequilibrium in this market

--Disequilibrium occurs whenever there is excess demand or supply in a market.

What are the main characteristics of a market economy?

Can you explain the concept of perfect competition within a market system?

What are the differences between a market economy and a planned economy?

How do prices get determined in a market system?

What role do entrepreneurs play in a market economy?

What are some examples of market systems in the real world?

How does supply and demand influence a market system?