ECO-Price elasticity of demand, page no 71

What is price elasticity of demand:

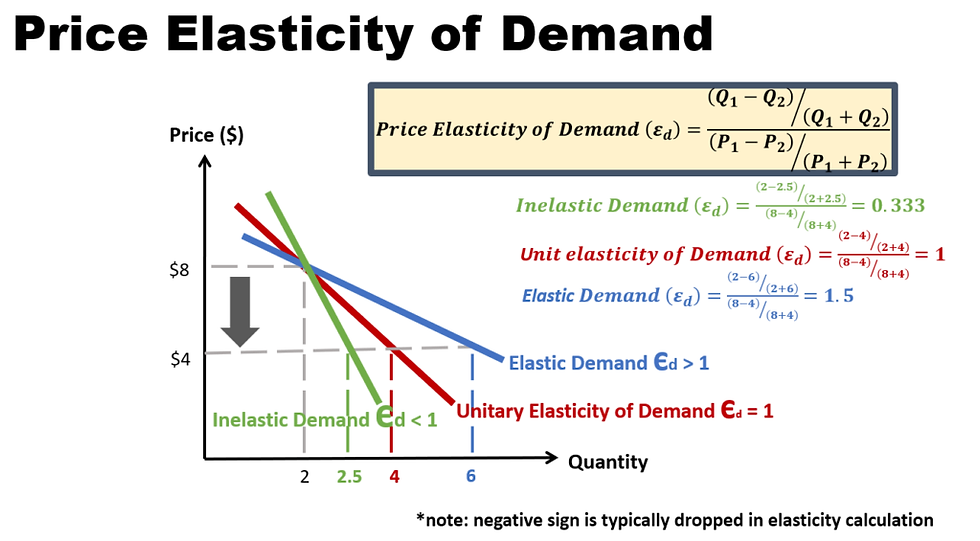

Price elasticity of demand measures how sensitive the quantity demanded of a good or service is to changes in its price. Specifically, it quantifies the percentage change in quantity demanded resulting from a one-percent change in price. If a product is elastic, a small price increase can lead to a significant drop in demand, while a price decrease may result in a substantial increase in quantity demanded. Conversely, inelastic demand indicates that changes in price have a minimal effect on quantity demanded. For example, necessities like food and medicine typically have inelastic demand because consumers need them regardless of price changes, while luxury items, such as high-end electronics, tend to have elastic demand since consumers can forego purchases when prices rise. Understanding price elasticity helps businesses and policymakers make informed decisions regarding pricing strategies, taxation, and market regulation, ultimately influencing revenue and consumer behavior.

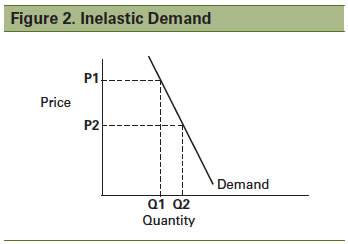

What is price inelastic demand:

Price inelasticity of demand refers to a situation where the quantity demanded of a good or service is relatively unresponsive to changes in its price. In other words, when the price of an inelastic good rises or falls, the demand for that good changes very little. This characteristic is typically observed in essential goods, such as basic food items, fuel, and medical care, where consumers will continue to purchase them despite price fluctuations. Price inelasticity is measured using the price elasticity of demand coefficient, which is less than one for inelastic goods. For instance, if the price of gasoline increases, consumers may reduce their consumption slightly, but they will still need to purchase fuel for their vehicles. This inelastic nature often leads to greater revenue for producers when prices increase, as the slight decrease in quantity demanded does not offset the higher prices. Understanding price inelasticity is crucial for businesses and policymakers, as it influences pricing strategies, tax policies, and market predictions. For example, if a customer is planning a vacation and the price of airline tickets is too high, they may choose to delay their trip or look for alternative ways to get to their destination.

THE END

What is the difference between elastic, inelastic, and unitary elastic demand?

How does the time period affect the price elasticity of demand?

How does the availability of substitutes affect the price elasticity of demand?

How do consumer habits and brand loyalty contribute to price inelastic demand?

What role does time play in determining the price elasticity of demand for a product?

How can businesses leverage knowledge of price inelastic demand in their pricing strategies?

What are the implications of price inelastic demand for government taxation policies?